Here’s a video on Mutual of Omaha Cancer Insurance:

Cancer is a diagnosis no family ever wants to face, yet the reality is unavoidable. According to national statistics, nearly 1 in 3 women and 1 in 2 men in the United States will be diagnosed with cancer during their lifetime. Even as medical technology improves and survival rates continue to rise, one critical challenge remains unchanged: cancer is expensive.

For many households, the financial strain of cancer can be just as overwhelming as the physical and emotional toll. This is exactly why more Americans are turning to Mutual of Omaha Cancer Insurance a cash benefit policy designed to protect families from the hidden and uncovered costs of a cancer diagnosis.

In this comprehensive guide, we’ll explore how Mutual of Omaha Cancer Insurance works, why it’s so important today, how it compares to Heart Attack/Stroke Insurance and Critical Illness Insurance, and why Critical Illness coverage typically costs more. We’ll also review real customer stories, state availability, and why Mutual of Omaha remains one of the most trusted names in insurance.

Why Cancer Insurance Matters More Than Ever

A cancer diagnosis impacts far more than hospital bills. While major medical insurance may cover treatment, patients are often left exposed to countless non-medical and out-of-pocket expenses, including:

- Lost income due to time away from work

- Childcare or elder care expenses

- Travel costs to specialized treatment centers

- Parking, lodging, and meals during treatment

- Prescription drugs are not fully covered

- Special diets and nutritional support

- Ongoing household expenses like mortgage, rent, utilities, and groceries

According to the National Cancer Institute, the economic burden of cancer reached $21.09 billion in 2019, with nearly $16.22 billion paid directly out-of-pocket by patients. Even those with strong employer-sponsored health plans often face high deductibles, copays, and coinsurance.

This financial pressure is where Mutual of Omaha Cancer Insurance becomes a lifeline.

How Mutual of Omaha Cancer Insurance Works

Unlike traditional health insurance, Cancer Insurance pays benefits directly to you, not to hospitals or doctors. Upon a covered cancer diagnosis, policyholders receive a tax-free lump-sum cash benefit.

There are no restrictions on how the money is used. No receipts. No reimbursement paperwork. No waiting for approvals.

Policyholders commonly use benefits for:

- Medical deductibles and copays

- Income replacement while unable to work

- Mortgage or rent payments

- Childcare or in-home assistance

- Travel to treatment facilities

- Home cleaning, meal preparation, or other support services

- Any personal or household expense

This flexibility allows families to focus on recovery, not finances.

Coverage Designed for Today’s Families

Mutual of Omaha has designed its Cancer Insurance to be simple, flexible, and accessible, making it suitable for young adults, families, and retirees alike.

Flexible Benefit Amounts

Coverage options typically range from $10,000 to $100,000, allowing consumers to tailor protection to their financial responsibilities and risk tolerance.

Coverage Options

- Individual coverage

- Single-parent coverage

- Family coverage

Coverage Duration Choices

- Lifetime coverage (benefits never expire)

- Term options: 10, 15, 20, or 30 years (availability varies by state)

Simple Underwriting

- Coverage up to $50,000 requires only three medical questions

- No medical exam required

This streamlined process makes coverage attainable even for older applicants or those with minor health concerns.

Understanding Heart Attack & Stroke Insurance

Heart disease and stroke remain among the leading causes of death and disability in the U.S. Mutual of Omaha’s Heart Attack & Stroke Insurance provides a lump-sum cash benefit if the policyholder experiences a covered cardiac or cerebrovascular event.

These benefits can help cover:

- Emergency medical costs

- Rehabilitation and physical therapy

- Time away from work

- Home modifications

- Ongoing household expenses

This coverage is more limited in scope than Critical Illness Insurance, focusing specifically on heart attack and stroke events, which is why it generally costs less than Critical Illness coverage.

Why Critical Illness Insurance Costs More

Critical Illness Insurance is the most comprehensive option within Mutual of Omaha’s Critical Advantage Portfolio, and it typically costs more for a simple reason: it covers more conditions.

Critical Illness policies often include protection for:

- Cancer

- Heart attack

- Stroke

- Major organ failure

- Kidney failure

- Organ transplant

- Paralysis

- Coma

- Severe burns (state-specific)

Because the likelihood of experiencing any one of these conditions is higher than experiencing cancer alone, insurers assume more risk, resulting in higher premiums.

In short:

- Cancer Insurance: Targeted, condition-specific, lower cost

- Heart Attack & Stroke Insurance: Focused coverage, moderate cost

- Critical Illness Insurance: Broad coverage, higher cost due to expanded protection

Many families choose to layer policies for maximum protection and affordability.

Sample Pricing Scenarios

Below are real pricing examples. These examples help illustrate how costs may vary based on age, state, and the type of plan you choose. Rates can change by location and time, so these are for illustration only.

Sample Scenario #1

- State: Florida

- Coverage Type: Individual

- Age: 60 years old

- Term: Lifetime Benefit

- Premium Mode: Monthly

| Plan | Benefit Amount | ||||

| $10,000 | $20,000 | $30,000 | $40,000 | $50,000 | |

| Cancer | $16.90 | $34.80 | $52.70 | $70.60 | $88.50 |

| Heart Attack and Stroke | $14.30 | $29.60 | $44.90 | $60.20 | $75.50 |

| Critical Illness | $44.00 | $89.00 | $134.00 | $179.00 | $224.00 |

NOTE: Critical Illness Insurance is only offered to applicants age 64 and under.

Sample Scenario #2

- State: Vermont

- Coverage Type: Individual

- Age: 48 years old

- Term: Lifetime Benefit

- Premium Mode: Monthly

| Plan | Benefit Amount | ||||

| $10,000 | $20,000 | $30,000 | $40,000 | $50,000 | |

| Cancer | $8.20 | $17.40 | $26.60 | $35.80 | $45.00 |

| Heart Attack and Stroke | $7.10 | $15.20 | $23.30 | $31.40 | $39.50 |

| Critical Illness | $21.80 | $44.60 | $67.40 | $90.20 | $113.00 |

NOTE: Critical Illness Insurance is only offered to applicants age 64 and under.

Sample Scenario #3

- State: Maine

- Coverage Type: Individual

- Age: 35 years old

- Term: Lifetime Benefit

- Premium Mode: Monthly

| Plan | Benefit Amount | ||||

| $10,000 | $20,000 | $30,000 | $40,000 | $50,000 | |

| Cancer | $5.08 | $11.17 | $17.25 | $23.33 | $29.42 |

| Heart Attack and Stroke | $4.60 | $10.20 | $15.80 | $21.40 | $27.00 |

| Critical Illness | $13.80 | $28.60 | $43.40 | $58.20 | $73.00 |

NOTE: Critical Illness Insurance is only offered to applicants age 64 and under.

Real Customer Stories That Prove the Value

Roger’s Story

Roger, age 62, was the sole income earner in his household with limited savings. He purchased a $10,000 Cancer Insurance policy because it was simple and affordable.

Years later, when he was diagnosed with cancer, the cash benefit helped cover expenses his health insurance didn’t allow him to continue working as long as possible, and avoid financial collapse.

Jean’s Story

Jean, 61, had witnessed loved ones struggle financially during illness. She chose a Critical Illness policy with cancer coverage and a return-of-premium option. No medical exam was required.

Her decision was proactive and grounded in one belief: insurance can’t prevent illness, but it can prevent financial disaster.

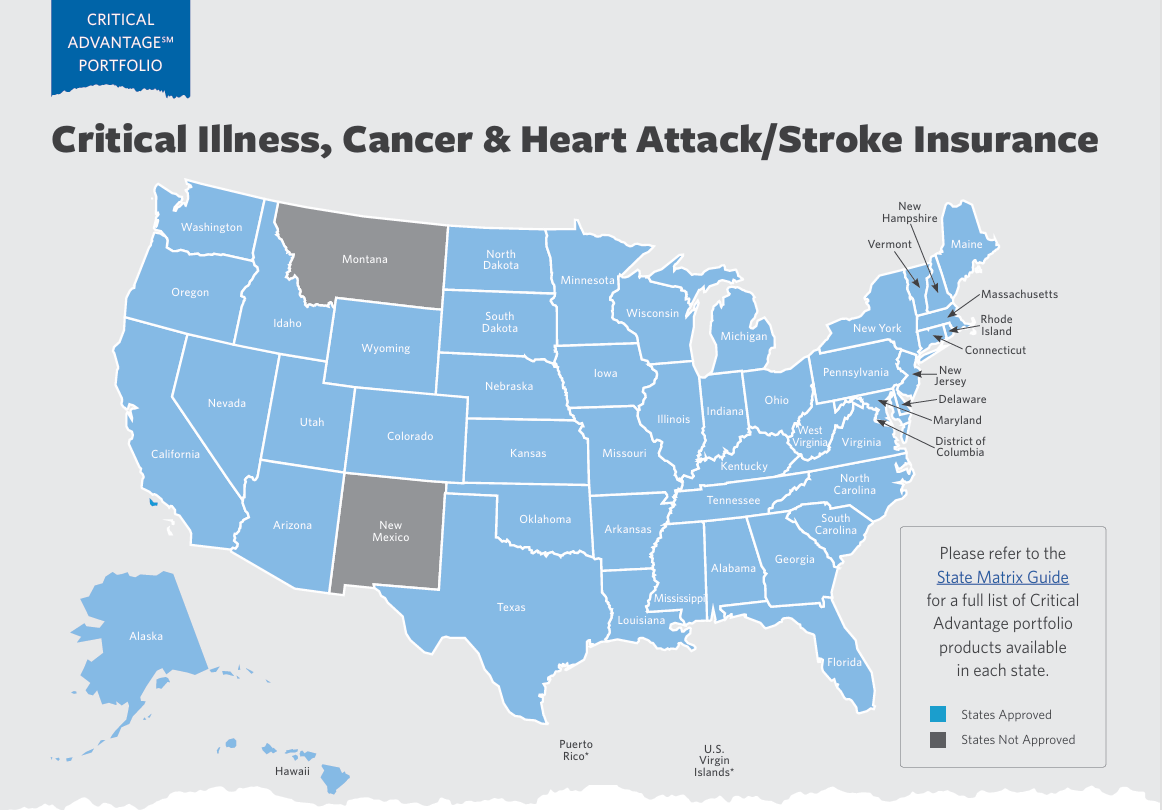

State Availability of Mutual of Omaha Cancer Insurance

Not Approved In:

- Montana

- New Mexico

- Puerto Rico (advisor-only)

- U.S. Virgin Islands (advisor-only)

States With Unique Restrictions:

- No term coverage: CT, ME, MN, NH, NJ, NY, UT, VA

- No cash value rider: AZ, DE, GA, ID, IA, PA, TX, WA

- Limited definitions or riders: NJ & NY

Some states may also require:

- Active health insurance

- Consumer acknowledgment forms

- Additional disclosures

To make it easy to see where Mutual of Omaha Cancer Insurance is available, check the map below for its availability. The map provides a quick visual reference by state, helping you understand where coverage is approved or restricted. Our licensed agent can confirm availability in your ZIP code.

Why Consumers Trust Mutual of Omaha

Mutual of Omaha has been helping families since 1909. It is a mutually owned company, which means it works for its policyholders, not shareholders. The company is known for strong financial stability and reliable service. Mutual of Omaha has earned high ratings from top agencies for its ability to pay claims. These ratings show that help is there when people need it most.

Financial strength ratings include:

- A+ (Superior) – AM Best

- A1 – Moody’s

- A+ – S&P Global

These ratings reflect exceptional claims-paying ability when policyholders need it most.

Mutual of Omaha Cancer Insurance pays a cash lump sum if you are diagnosed with cancer. This money is paid directly to you, not the doctor or hospital. You can use it for medical bills, travel, or everyday expenses. This support helps you focus on healing and recovery.

For more than 50 years, Mutual of Omaha’s Wild Kingdom shared a message about protection. Just like animals protect their own, people want to protect what matters most. Mutual of Omaha helps protect lives, families, and futures through insurance and financial products. This long history builds trust and peace of mind.

Who Should Consider This Coverage?

Mutual of Omaha Cancer Insurance is ideal for:

- Individuals with high-deductible health plans

- Families dependent on one income

- People with a family history of cancer

- Retirees and pre-retirees on fixed incomes

- Anyone seeking financial stability during health emergencies

Optional Riders for Enhanced Protection

To further customize coverage, Cancer Insurance offers optional riders. These riders help cover more health events and give added peace of mind. You can choose the riders that fit your needs best.

Heart Attack and Stroke Benefit

This rider pays a lump-sum amount if you have a heart attack or a stroke. It can also pay if you need heart surgery, like bypass or angioplasty. The money is paid directly to you. You can use it for medical bills or daily expenses.

Cash Value Benefit

This rider helps if you worry about paying for a policy you may never use. It can return a percentage of the premiums you paid over time. Any benefits already paid are subtracted from this amount. This rider adds an extra layer of security and peace of mind.

NOTE: Additional premium applies. Policy benefits and features may not be available in all states.

Final Thoughts

Cancer, heart attacks, and strokes can happen without warning. These events can be scary, but money worries do not have to make them worse. Mutual of Omaha Cancer Insurance helps by paying cash directly to you. This money can be used for medical bills, travel, or daily needs. It gives families peace of mind during a hard time.

Having the right coverage helps protect your future. It lets you focus on getting better instead of stressing about costs. Connect directly with one of our trusted agents to start. Give us a call at 1-888-559-0103 or Set an Appointment with Eric Rosenberg or Jackson Edwards.