Do I Need Medicare Supplemental Insurance?

With all of the Medicare plan options out there, many people may wonder, “Do I need to purchase Medicare supplement insurance?” This is a common question, especially among new seniors, because everyone wants to find what best fits them.

Once you sign up for traditional Medicare, you will soon learn that it is not as broad as traditional health insurance you may have had from an employer or through a privately purchased plan.

Traditional Medicare has two basic parts:

Part A is basically hospital insurance. It will cover inpatient hospital stays, hospice care, skilled nursing care, and limited home healthcare services. You will often have to pay a deductible and coinsurance and or copayments.

Part B is more like medical insurance. It generally covers services and items such as:

- Doctor office visits

- Preventive services, such as certain tests and screenings

- Flu shots

- Pneumococcal shots

- Mental health care (outpatient)

- Alcohol use counseling

- Chemotherapy

- Physical therapy

- Diabetes screenings, supplies, and self-management therapy

- Durable medical equipment, such as wheelchairs

This list is not exhaustive. There are other services B will provide, but certain coverage rules will apply. You can find a complete list at Medicare.gov. If you see a medical provider who deems certain items and or services are medically necessary, these can also be covered. Your healthcare provider is another good resource to help you sort through Part B coverages.

Remember that under Part B, in most cases you will pay 20% of the Medicare-approved amount for each item or service. A deductible may also apply. Medicare also has Part C and D. Part C is Medicare Advantage and Part D is Medicare’s prescription drug coverage. But the focus of this article is the traditional A & B plans.

When you look at this list, you probably wonder why you would need something to supplement coverage that seems so broad. Medicare is great coverage, but there are gaps that could cost you more than you expect. The deductibles and co-pays can also be expensive. That is why considering a supplement is a good idea.

What is Medicare Supplement Insurance

In order to enroll in a supplement Medicare plan, you need to be enrolled in Medicare plans A and B. If you are not enrolled in these plans, you cannot receive Medicare supplement insurance. While Medicare plans A and B are great, they have some gaps where you may not be covered. In the event of an incident, you could pay more out of pocket unless you have a Medicare supplement. Medicare supplements cover many of the gaps that plan A and B do not cover.

If you have Medicare plans A and B but no supplement plan, some costs will quickly add up. For instance, if you are hospitalized for more than 60 days, you will begin to pay more. If you are hospitalized for more than 120 days, you lose coverage. These costs can be avoided if you have a supplement plan. Medicare Supplement products are designed to fill in the gaps.

What is Not Covered Under Medicare Plans A and B?

You may wonder what is not covered under Medicare plans A and B. There are some situations when it is wise to have supplemental insurance.

If you are a frequent international traveler, Medicare plans A and B may not cover hospitalizations abroad. Depending on the supplement plan, these visits could be covered up to 80% of the total cost. Supplements are also helpful if you are frequently hospitalized or frequently visit a healthcare professional. Only 60 days in the hospital are covered under plans A and B. A supplement plan would cover hospitalization after this period.

Other services not covered under plans A and B are dental, eye care that requires fitting new glasses, dentures, cosmetic surgery, acupuncture, hearing aids and foot care. All of these services can be covered through supplements. If you frequently require coverage for these services, a supplement plan may be the best option.

Here is a real-life example to help understand the impact of these Medicare gaps.

Hospitalization Gaps:

Susan is covered by traditional Medicare under Parts A & B, but she doesn’t own a supplement product. One day, she begins to feel dizzy and her speech starts to slur. Her arms feel weak. Her husband is close by and notices the changes. He calls their doctor and immediately gets her into the car and heads toward the nearest emergency room.

Upon arrival at the emergency room, it is apparent to the providers that Susan is having a stroke, and must be immediately admitted. Medicare pays for action taken to save her life and stop further damage to her brain by stopping the stroke. Unfortunately, Susan will still have a large out-of-pocket expense for her time in the hospital. She will have to pay close to $13,000 in hospitalization expenses that aren’t covered by Part A.

If the hospitalization is extended for more than 60 days, she will have to pay a portion each day she is in the hospital. Costs continue to incur the longer she stays in the hospital.

Primary Doctor Gaps:

Fred regularly visits a doctor to manage his blood pressure and diabetes. Under Medicare, his deductible is $147. Then under Part B, he is required to pay 20% of the Medicare-approved amount.

That sounds cheap. But what if his medical expenses total $100,000 or more? If you have ever received any type of surgery or medical care, you realize that costs can skyrocket. Even with a 20% out-of-pocket expense, in this case, Fred would owe a minimum of $20,000.

There’s no limit on the amount of those expenses. And those costs are enough to bankrupt many people, especially when you are on a fixed income.

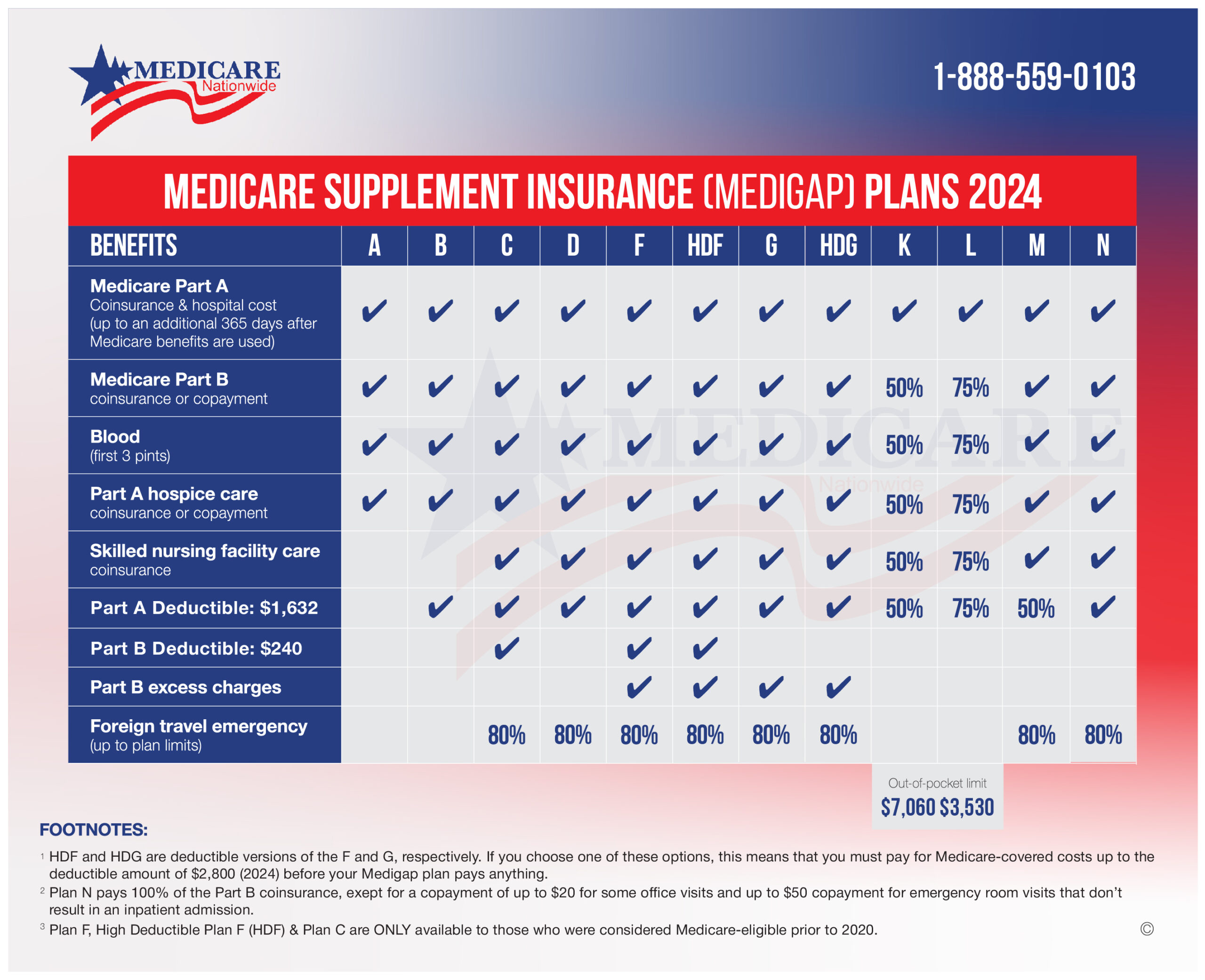

Medical Supplement coverage is designed to pick up those extra expenses that Medicare will not cover. To protect consumers, the supplement plans have been standardized by the U.S. government, which mandates the coverage details of each plan. Each plan is designated by a letter code such as Plan A, B, C, F, G, etc.

Plan A is the most basic plan you can purchase. All other plans build off of Plan A. The two most comprehensive plans available are Plan F & G.

Here’s a visual guide we use often to help our customers understand what each plan offers and how they fill the gap Medicare does not cover.

As the supplement comparison chart shows, each plan covers specific gaps. That’s why it is a wise decision to consider supplementing what traditional Medicare offers.

Is There Open Enrollment for Medicare Supplements?

Yes. There is open enrollment for Medicare supplements. The best time to purchase Medicare Supplement insurance is during the open enrollment period. There is a six-month window that begins on the month of your 65th birthday and extends for five more months. During that period, the government guarantees you can purchase any Medicare Supplement plan available in your state.

Unlike traditional health insurance companies that can deny coverage based on pre-existing conditions, companies offering Medicare supplements cannot deny coverage based on pre-existing conditions during the enrollment window.

Your health status does not matter during the enrollment window. Insurance companies ignore pre-existing conditions during this time. If you have ever tried applying for health coverage or even life coverage, you understand the importance of this benefit. Waiting for acceptance is stressful, because of testing and questions during the underwriting period. This is eliminated during the acceptance window.

What if you don’t enroll during the enrollment window?

You can always purchase a supplement product outside the enrollment window, but you could be denied coverage because of health issues. You will also be subject to higher premiums based on your health. It is critical to purchase a policy during this window. The benefits outweigh the risks of waiting.

That’s no problem. You are in the system, and as long as you maintain coverage you can change companies and shop for different plans and benefits. Enrolling during the window is the secret.

Can You be Denied Medicare Supplemental Insurance?

You cannot be denied Medicare. It is available to all Americans over the age of 65. But you can be denied a supplement. If you purchase within the available window when you turn 65, you will not be denied. If you wait, there is the potential you will struggle to find coverage or at least affordable coverage.

During the Guaranteed Issue period, you will have limited time to enroll in a Medicare plan and supplement without needing an underwriting review. Guaranteed Issue periods also include moving out of the geographic area in which you are covered. Both of these conditions allow you to enroll in Medicare without the chance of denial. Unless you are in these two circumstances, you will need to undergo an underwriting review that could lead to a denial. A denial by one company does not mean there are other insurance companies that will not offer coverage.

Our experienced team specializes in finding coverages for people that find themselves in this situation. Each company has different underwriting requirements and what may create a denial for one company will not be the same for another. If you are in that situation, you can still find help.

United Healthcare’s New Program – Renew Active

Despite the partnership between SilverSneakers and United Healthcare ending, United Healthcare is promoting fitness for seniors with a new program.

Renew Active

Renew Active is a new program that is covered by United Healthcare to promote the same fitness goals seniors have been achieving through SilverSneakers.

Along with typical workout routines, Renew Active provides brain fitness activities. This program, known as AARP Staying Sharp, comes at no additional cost to subscribers who already receive Renew Active as a benefit. Staying Sharp allows users to take a quiz that builds a personalized routine. Articles on mental fitness and workouts are all provided virtually.

Renew Active provides many of the same benefits as SilverSneakers. Gyms are available to members at no additional cost with instruction-based classes and open gym equipment. Renew Active also offers a FitBit sponsored community in which members can track their progress with other members, supporting the social aspect of this program.

Regardless of your fitness level, you can find programs that fit your needs. Here are some examples of programs available:

- Strength programs including dumbbells, kettlebells, resistance bands, calisthenics

- Aquatic programs such as water yoga, aqua aerobics, and swimming

- Cardio such as cycling, kickboxing, and aerobics.

- Specialty programs such as personal training, Zumba, and self-defense

- Mind/Body activities like yoga, pilates, and tai chi

If you are worried about transitioning to Renew Active, check out fitness locations in your area. Their simple locator service will give you all the resources you need.

Renew Active locator

When any company changes programs, it can cause doubt or stress for current policyholders or for those considering a new company. We believe the programs United Healthcare has created are comparable to Silver Sneakers. But if you are committed to the Silver Sneakers program, we can help you compare Medicare Supplement plans with that benefit.

Many of our other companies offer Silver Sneakers, and letting us run a comparison will help you decide which plan is the best fit for your needs and budget.

Prefer to chat by phone? Give us a call at 1-888-559-0103.