Company Backstory

ManhattanLife is an old company. They were incorporated on May 29, 1850, as an upcoming life insurance company. Their first President was an entrepreneur who had worked as a hat maker, politician, and insurance agent.

ManhattanLife creatively structured the company to create consumer confidence and ensure financial health. At least half of the board of directors had to be a policyholder with premiums of at least $100 per year.

Also, any policyholder whose premiums were greater than $75 was able to vote. This unique move and structure established the foundation for success and security. It also provided a model for future financial organizations.

In 1854, they issued their first group policy to a company transporting 700 immigrants by ship to the United States. After the Civil War, ManhattanLife was known as “Old Reliable”. They contributed to the healing of the country, by paying death benefit claims to the widows of Southern soldiers. For many years, their headquarters in New York was the tallest building in the city.

In recent years, ManhattanLife moved its headquarters to Houston and is part of the Manhattan Life Insurance Group. The Manhattan Group includes Central United, Western United, and Family Life. Each one of the subsidiaries also offers a Medigap plan, but they could vary by where you live.

Apart from the generic Medicare supplement plans, you have the option to extend your coverage with accident insurance, cancer insurance, hearing, dental, vision insurance, and disability coverage.

A.M. Best has given ManhattanLife a B+ rate as of 2022, which means their rating is stable but not as strong as some of their larger competitors.

Medigap Plan Products and Features

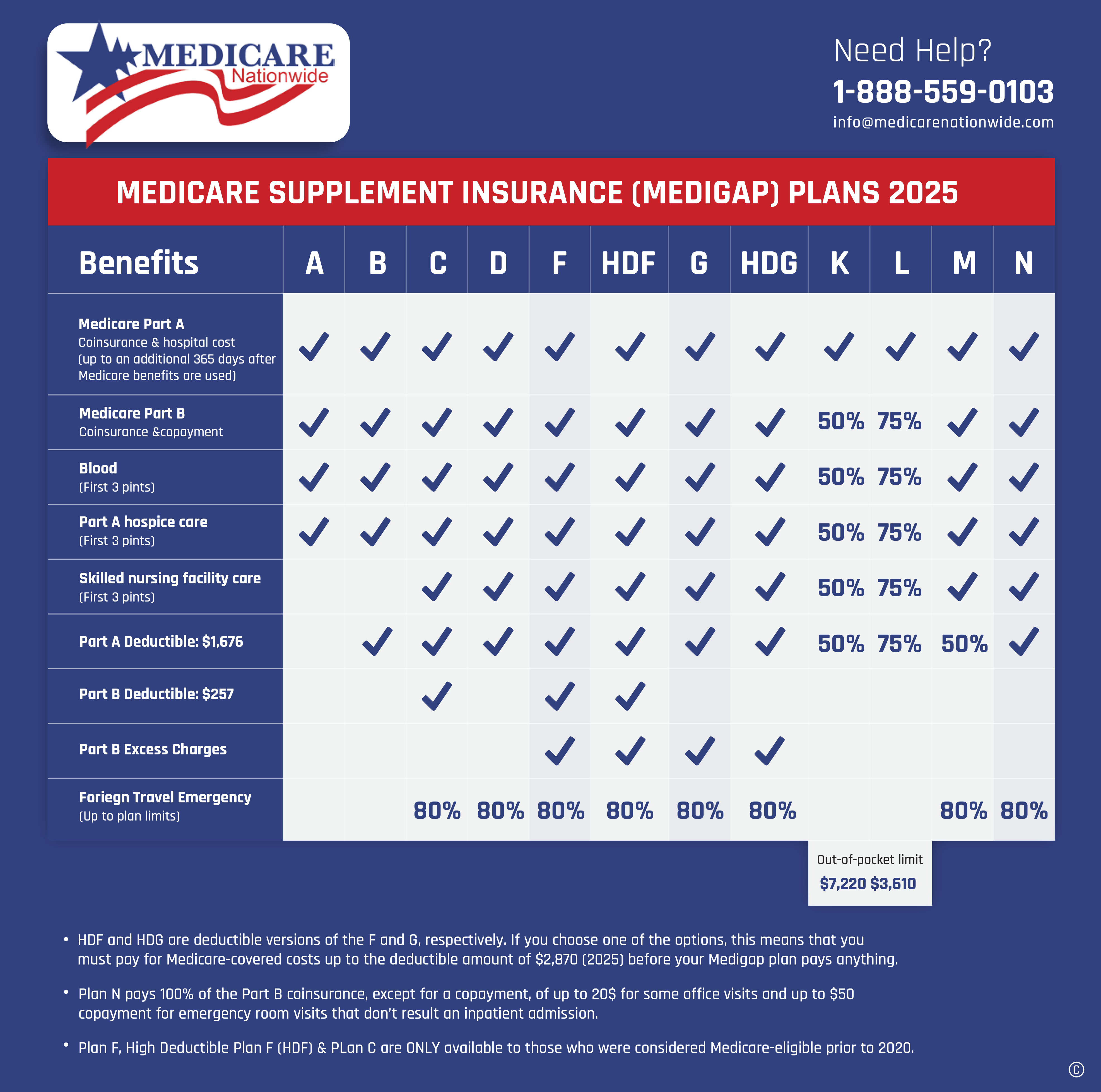

ManhattanLife offers 5 of the available Medicare Supplement plans. These are Plans A, C, F, G, & N.

Like other companies, the federal government mandates the benefits of the plans. Understanding the framework of the overview Medicare Supplement can help us narrow down our choices of plans.

Here is a brief summary of the details and benefits of each plan:

Medicare Supplement Plan A

- Medicare Part A hospital coinsurance

- Medicare Part A supplemental hospital care (additional 365 days after Medicare benefits end)

- Medicare Part A coinsurance for hospice care

- Medicare Part B coinsurance for hospital outpatient services (generally 20% of costs approved by Medicare)

- First 3 pints of blood each year

Medicare Supplement Plan C

- Plan C provides all the basic benefits of Plan A with these extra benefits:

- Part A hospital deductible for inpatient services

- Skilled nursing facility coinsurance (for days 21 – 100)

- Part B deductible for qualified medical and hospital services, generally for outpatient services

- Foreign travel medical emergency coverage

Medicare Supplement Plan F

- Plan F includes the basics of Plan A and also the most complete collection of Medicare Supplement coverages available. It covers 100% of all Medicare gaps.

- Part A hospital deductible for inpatient services

- Skilled nursing facility coinsurance (for days 21 – 100)

- Part B deductible for qualified medical and hospital services, generally for outpatient services

- Part B excess charges benefit for charges exceeding the normal Part B limit

- Foreign travel medical emergency coverage

Medicare Supplement Plan G

Plan G provides all of the basic benefits of A plus extra coverage for hospitalization, but not the Part B deductible. Next to Plan F is the second most comprehensive plan. Often the savings on this plan will fund any deductible you might pay.

- Part A hospital deductible for inpatient services

- Skilled nursing facility coinsurance (for days 21 – 100)

- Part B excess charges benefit for charges exceeding the normal Part B limit

- Foreign travel medical emergency coverage

If you are interested in Plan F, you should get quotes on Plan G as well.

Medicare Supplement Plan N

Plan N is becoming more popular because many consumers are willing to absorb copays for a lower premium. Premiums are lower than G, with similar benefits. You do agree to pay some doctor copays and the Part B Deductible which lowers the cost. Here are the benefits:

- Part A coinsurance (generally 20% of costs approved by Medicare) – for hospital outpatient services

- Part B hospital deductible for inpatient services is covered. You are only responsible for a $50 ER copayment and/or a $20 copayment for a doctor’s office visit.

- Skilled nursing facility coinsurance (for days 21-100)

- Foreign travel medical emergency coverage

Manhattan Life Medicare Supplement Pricing

Many of our customers find ManhattanLife very competitive. ManhattanLife offers a 7% household discount on their Medicare Supplement insurance. A married couple or any two people who live together and are over 60 years old will qualify. Remember there may be states where the discount is not available such as Ohio. If you are interested in ManhattanLife, it can be difficult to find pricing on their site. We have access to their rates and can run your numbers on their products. Because they tend to be competitive, they are often a company we offer in our quote comparisons.

- Plan A: $96.08

- Plan F: $111.75 (must be grandfathered in)

- Plan G: $90.75

- Plan N: $70.85

*The rates above are based on zip code 24531 in Pittsylvania County, Virginia. These rates are subject to change and are illustrative in nature for a 65 female. Rates vary widely by demographics and location.

Manhattan Life Reviews and Ratings

You can learn how well-regarded rating platforms compare an insurer’s supplement overview, medicare quality, and customer success rate to those of the competitors. Watch how ManhattanLife’s Medicare Supplement plans are rated by Demotech, A.M. Best, and the Better Business Bureau.

A.M. Best is a credit rating company with a focus on the insurance sector. A.M. has given a B+ ranking to the carrier in this category. Thus implying that ManhattanLife will be able to fulfill its insurance commitments with reasonable ease. Ratings from the Better Business Bureau (BBB) offer insight into how well a company is likely to deal with its clients.

After a comprehensive Medicare Supplement overview, The Better Business Bureau has given ManhattanLife Group an A+ rating and accreditation status since 2013. Thirty-nine consumer complaints have been reported to and handled by the BBB in the last three years. None were particular to the Seniors’ Lighthouse Series or the supplement insurance plans.

All sizes of insurers proudly carry their financial stability ratings from Demotech. Demotech confirmed that all of ManhattanLife’s affiliated companies received an A(exceptional) rating for financial stability in September 2021.

Medicare Advantage Plans – Manhattan Life

Medicare Advantage Plans are not available from Manhattan Life. These plans, which take on the role of Original Medicare, are typically network-based.

Manhattan Life Part D Medicare plans

Manhattan Life Solutions does not provide Part D plans. If you need assistance choosing the appropriate medicare products for the prescriptions you are taking, please give us a call. Our insurance producer would be happy to help.

What Makes Manhattan Life different and gives you an Advantage?

You can count on Manhattan Life Group for very good customer service. They have an A+ rating with the Better Business Bureau (BBB). Many companies will underwrite your health history aggressively, which could cause much higher rates. You may even be declined for coverage. If you are searching for a new company with more competitive rates, this can be a problem. Not for ManhattanLife. As long as you only have one “Yes” answer to health issues, you can still be written with ManhattanLife. Tests for blood thinners and routine glucose testing are generally accepted, as long as their overview doesn’t indicate serious illness.

Consistency

ManhattanLife has a strong track record of stability. The organization now has a B+ (“excellent”) grade from the rating company AM Best, which shows that it is more than capable of upholding its coverage commitments. As dictated by a wholesome insurance overview, accident, cancer, and critical illness insurance policies have truly been a lifesaver for many American policyholders.

Over 170 years have passed since it began serving customers in the USA. The stability and duration of the company’s history are unquestionably positive indicators when you’re seeking to select one that will match your needs.

Discounts

Families with two members who each have a ManhattanLife Medicare Supplement plan are eligible for a Household discount. For example, up to 7% discount in Pennsylvania. If you had a policy that cost $150, you could save $10 per month or $120 annually if you did this. One should note that eligibility for this discount varies by the state due to the mandates imposed by the Dept. of Insurance in that particular state. In some states, this discount also goes up to 12%.

Ask the agent if there are any further discounts available in your region when you chat with them.

Health Qualifications

Here is a list of conditions that would have caused a declination prior to this year. However, if you have been treated for any in this list, ManhattanLife will consider your application.

- Coronary Artery Disease

- Angina

- Heart Attack

- Aortic Cardiac Aneurysm

- Peripheral Artery Disease

- Peripheral Venous Thrombotic Disease

- Vascular Angioplasty

- Endarterectomy

- Carotid Artery Disease

- Internal Cancer Leukemia

- Melanoma

- Hodgkin’s Disease

- Lymphoma

- Cardiac Angioplasty

- Bypass Surgery

- Stent Replacement

- Cardiomyopathy

- Congestive Heart Failure

Diabetics using an insulin pump with kidney disease or using dialysis will not be accepted. Strokes or pulmonary issues also are rejected. The regular use of medication containing narcotics is accepted. These are medicines such as Oxycodone, Oxycontin, Fentanyl, etc.

Tobacco users are considered a higher risk for future health risks.

Because of this, ManhattanLife is stricter than many companies regarding tobacco use. To receive their preferred rates, you must be a full 5 years without any tobacco use. If you have been tobacco-free for 5 years, you can be re-rated to Preferred rates. Be ready to fill out a tobacco questionnaire, and have it confirmed by your family doctor.

Applicants with recent surgery are not a problem if all follow-up treatment has been completed. You will also need verification from your doctor that you have been released from surgical care.

Claims Experience

Medicare is the final arbiter on whether claims are paid or not. But it is important that the carrier you choose has efficient claims processes. You also want a company that makes reporting claims very easy.

ManhattanLife Insurance has consistently high reviews regarding all their claims processes. Medicare rating agencies give Manhattan life 3.5 out of 5 stars.

Other Products

Manhattan Life doesn’t only sell Medicare Supplement plans. They also sell:

- Accident Insurance

- Cancer Insurance

- Critical Care Insurance

- Dental Insurance

- Vision Insurance

- Disability Insurance

Manhattan Life Hearing, Dental, Vision & Other Benefits

In the majority of states, Manhattan Life provides dental, vision, hearing insurance, and similar policies for additional coverage as stand-alone plans (not included in Medicare supplement). Routine dental care is covered in the first year; dentures, bridges, and periodontal surgery are covered in the second year. You can purchase an eye exam, glasses, and contacts with the $1000 policy year maximum for vision coverage. The deductible for hearing insurance is $100. There is a 12-month waiting time for expensive hearing services.

Summary

Manhattan Life is a strong company with a long history of customer satisfaction. If you’ve had some health issues, Manhattan can be a good fit for life with competitive rates.

Next Steps

Don’t forget! The initial open enrollment period takes place the year you turn 65. It begins 3 months before your birth month and continues for another three months. The initial open enrollment is critical. An insurance company can not reject your application during this window, even if you have adverse health conditions. After this period, rates and acceptability can be much different.

Because we are a producer, we look at your unique situation and provide a range of quotes from multiple companies. It’s our job to find the best product for your insurance budget. We can help you arrange supplement overview, medicare quality comparison, and pricing bidding wars between similar companies in the industry because we know their history and experience with our other customers.

Contact us today

P. S. Also, remember Medicare Supplement overview does not include Medicare Part D drug coverage. We can help. During your coverage review, we will do an analysis of your ongoing medications. This assists us in finding the most cost-effective Prescription drug plan.

Prefer to chat by phone? Give us a call at 1-888-559-0103.