Medicare Supplement Plan C was once a top choice for those seeking broad coverage beyond Original Medicare. Though no longer available to new enrollees after 2020, many beneficiaries still maintain this robust plan. In this article, we’ll break down Plan C’s coverage, current costs, and available alternatives.

What Does Plan C Cover?

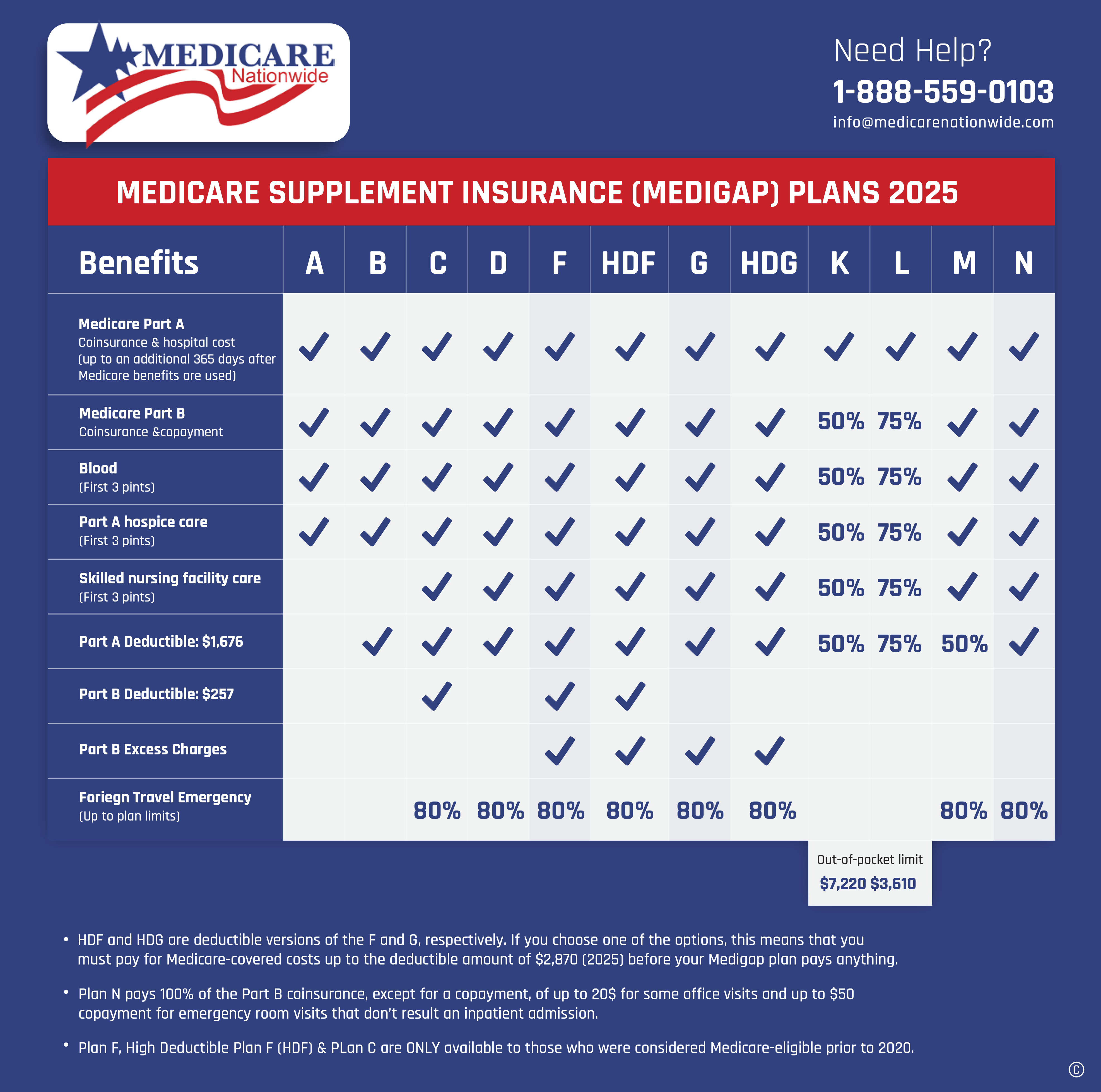

Plan C offered extensive coverage, including:

- Part A coinsurance and hospital costs: Covered the 20% coinsurance you typically pay for inpatient hospital stays and skilled nursing facility care. It even provided an additional 365 days of coverage after Medicare benefits ended.expand_more

- Part B coinsurance or copayment: Covered the 20% coinsurance or copayment for outpatient medical services and preventive care.expand_more

- Part A hospice care coinsurance: Covered the 20% coinsurance for hospice care.

- Skilled nursing facility care coinsurance: Covered the 20% coinsurance for skilled nursing facility care after the initial 20 days covered by Medicare.exclamation

- Blood (first 3 pints): Covered the cost of the first 3 pints of blood each year.expand_more

- Foreign travel emergency medical assistance: Provided limited emergency medical coverage while traveling outside the US.

Important Note: As of January 1, 2020, Plan C is no longer available to new beneficiaries. This means if you become eligible for Medicare on or after this date, you cannot purchase Plan C. However, if you enrolled in Plan C before 2020, you can generally keep your existing plan.

What Is Medicare Supplement Plan C and Who Is Eligible?

Medicare Supplement Plan C, also known as Medigap Plan C, was designed to help cover the “gaps” left by Original Medicare Parts A and B. It offered a comprehensive solution to out-of-pocket expenses such as copayments, coinsurance, and deductibles. However, eligibility for this plan has changed since 2020, and it’s important to understand who can still enroll.

As of January 1, 2020, Medigap Plan C is no longer available to individuals who became eligible for Medicare on or after that date. This change came from the Medicare Access and CHIP Reauthorization Act (MACRA), which prohibited Medigap plans from covering the Part B deductible for new beneficiaries. Since Plan C covers that deductible, it was discontinued for newly eligible enrollees.

If you were eligible for Medicare before January 1, 2020, you can still purchase Plan C if it’s offered by insurers in your state. If you’re already enrolled in Plan C, you’re allowed to keep your plan indefinitely. Understanding your Medigap Open Enrollment Period, the 6-month window after enrolling in Medicare Part B is crucial, as it guarantees coverage without medical underwriting.

This eligibility rule has caused many to consider alternatives like Medicare Supplement Plan G or Plan N, which offer strong benefits while still complying with current regulations.

Whether you’re new to Medicare or reviewing your options, knowing the status of Medigap Plan C and its historical coverage can help guide your decision-making.

Costs and Premiums for Medicare Supplement Plan B

Plan C premiums vary depending on several factors, including:

- Your age, location, and health status

- The insurance company you choose

- Any discounts or promotions offered

Since Plan C is no longer available to new enrollees, information about its current premiums may not be readily available. However, it’s important to remember that Medigap plans in general tend to have higher premiums compared to other Medicare options like Medicare Advantage plans.

Compare the Medicare Supplement Plan C average monthly costs across multiple U.S. cities, showing rates for both men and women at ages 65 and 75:

| Location | Gender / Age | Average Monthly Cost |

|---|---|---|

| Simpsonville, SC (29681) | Female, Age 65 | $188.60 |

| Male, Age 65 | $206.01 | |

| Female, Age 75 | $265.02 | |

| Male, Age 75 | $290.42 | |

| Saint Peters, MO (63376) | Female, Age 65 | $263.36 |

| Male, Age 65 | $288.62 | |

| Female, Age 75 | $356.37 | |

| Male, Age 75 | $389.78 | |

| San Francisco, CA (94112) | Female, Age 65 | $217.39 |

| Male, Age 65 | $217.39 | |

| Female, Age 75 | $318.15 | |

| Male, Age 75 | $318.15 |

Alternatives to Plan C

If you’re not eligible for Plan C, several other Medigap plans offer varying levels of coverage:

- Plan N: Covers most costs except the Part B deductible and excess charges.

- Plan G: Covers all the costs that Plan N does, plus the Part B deductible.

- Plan F: Covers all the costs that Plan G does, except for foreign travel emergency medical assistance (no longer available to new enrollees after June 2020).

Choosing the Right Medicare Plan

Selecting the right Medicare plan depends on your individual needs, budget, and health status. Consider factors like:

- Your expected medical expenses: If you anticipate extensive healthcare needs, a more comprehensive plan like Plan G might be suitable.

- Your budget: Medigap plans generally have higher premiums than Medicare Advantage plans, so factor in affordability.

- Your preferred network: Some Medigap plans offer broader network access than others.

Additional Resources:

- Medicare.gov: https://www.medicare.gov/medigap-supplemental-insurance-plans

- National Association of Health Underwriters (NAHU): https://welcometonahu.org

- State Health Insurance Assistance Programs (SHIPs): https://www.shiphelp.org